The Roth 401(k) vs. Traditional 401(k) Debate: What Most People Get Wrong

Contributing $24,500 to a Roth 401(k) and Traditional 401(k) isn't the same investment. A Charlotte, NC fee-only CFP® explains the math most people miss.

Contributing $24,500 to a Roth 401(k) and Traditional 401(k) isn't the same investment. A Charlotte, NC fee-only CFP® explains the math most people miss.

If you're a busy professional, maybe you're juggling equity compensation at a fast-growing company or running your own business, you've probably stared at your 401(k) enrollment screen and wondered: Roth or Traditional?

Most people think contributing $24,500 to a Traditional 401(k) and $24,500 to a Roth 401(k) means the same amount was invested.

It doesn't. And understanding why could change how you think about this decision entirely.

Let's walk through a simple example.

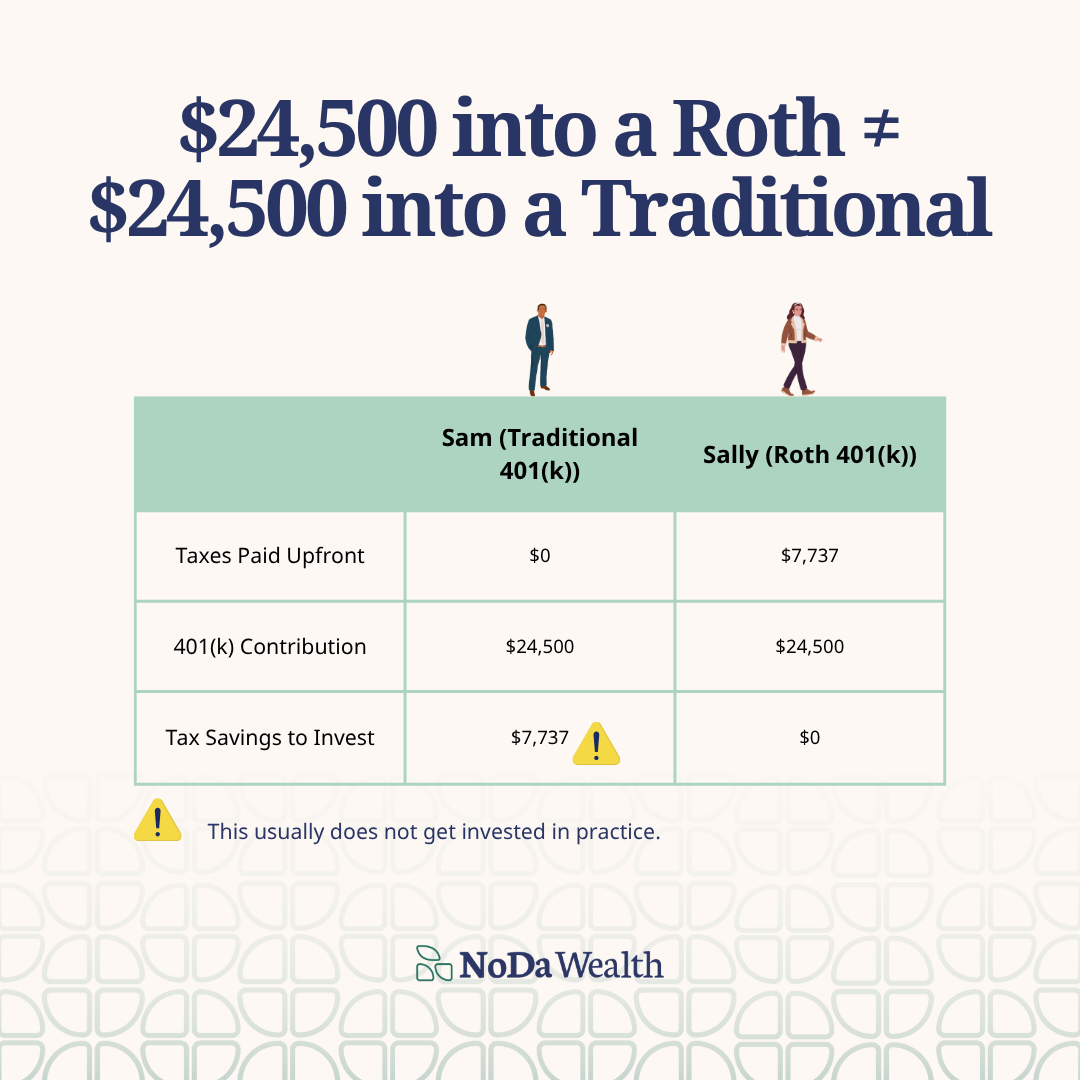

Sam contributes $24,500 to his Traditional 401(k).

Sally contributes $24,500 to her Roth 401(k).

Both are in the 24% marginal tax bracket.

Here's where it gets interesting. Sally had to earn $32,237 in gross income just to have $24,500 left after paying her 24% in taxes. That Roth contribution cost her more in real, pre-tax dollars than Sam's Traditional contribution cost him.

Sam, on the other hand, gets a tax deduction worth $7,737, the exact same $7,737 that Sally already paid in taxes to fund her Roth.

On the surface, it looks like Sam came out ahead. But here's the catch.

For the Traditional 401(k) to truly keep pace with the Roth on an apples-to-apples basis, Sam would need to take that $7,737 in tax savings and invest it, every single year, in a taxable brokerage account.

That's the part that rarely gets mentioned in the Roth vs. Traditional debate, and it's the part that matters most for real people living real lives.

On paper? Traditional can absolutely keep up if the tax savings are invested consistently and diligently.

In real life? That money often gets quietly absorbed into the daily chaos of life. A kitchen renovation. Summer camp tuition. A bigger vacation. A month where cash flow was tight and the tax refund felt like a windfall rather than an investment obligation.

If you're a professional with RSUs, stock options, or other equity compensation, your income can fluctuate significantly year to year. That makes the Roth vs. Traditional decision even more nuanced. In years when a large equity vest pushes you into a higher bracket, the Traditional deduction might carry more weight. In leaner years, Roth contributions could be the smarter play.

The point is: there's no autopilot answer. It requires planning.

Self-employed individuals often have access to Solo 401(k) plans or SEP IRAs, and many Solo 401(k) plans now allow Roth contributions. If you're running your own business, you're already wearing a dozen hats. The likelihood of manually investing your tax savings from a Traditional contribution into a separate brokerage account each year, on top of everything else, is, candidly, low for most people.

That behavioral reality matters. A plan that works on a spreadsheet but not in your life isn't really a plan.

I'd be doing you a disservice if I didn't mention this: the analysis above assumes your tax rate stays roughly the same in retirement. If you expect to be in a significantly lower bracket when you start taking withdrawals, which is entirely possible depending on your retirement income sources, the Traditional 401(k) can still win, and often does, even after accounting for the behavioral drag of reinvesting tax savings.

There are also scenarios involving state tax changes (North Carolina has its own tax considerations worth factoring in), future legislative risk, and the impact of Required Minimum Distributions that can tip the scales one way or the other.

It depends. I know that's not the satisfying, tweetable answer most people want. But it's the truth.

The "Roth Premium" is real. When you contribute to a Roth, you are putting more actual, after-tax dollars to work. That's not an opinion, it's math. But the right answer is always situational. It depends on your current tax bracket, your expected retirement bracket, your discipline with tax savings, your income variability, your state tax picture, and a dozen other factors unique to your family.

This is exactly the kind of decision that a comprehensive financial plan is built to answer, not with a guess, but with a projection tailored to your life.

Noda Wealth Management is a fee-only financial planning and investment management firm based in Charlotte, North Carolina. As a CFP® professional, I work with busy families navigating equity compensation and self-employed professionals who need a clear financial strategy. Fee-only means we don't earn commissions or sell products. Our only incentive is to give you the best advice possible.

Feeling overwhelmed? Let’s simplify things! Schedule your Free Assessment for an easy, 20-minute chat to help you tackle life’s transitions.

Enjoy a hassle-free conversation that puts your needs front and center!

)%20(3).avif)